Here are some recent Innovation Measurement web pages I have come across recently:

Boston Consulting Group (Aug. 2008)

Innovation 2008: Is the Tide Turning?

A survey of 3000 executives say they are less happy with their return on innovation (2008 43% happy, 2006 52% happy), and will spend less on innovation in 2008 (2008 63% spend more, 2006 72% spend more). 28 pages

http://www.bcg.com/impact_expertise/publications/files/Innovation_Aug_2008.pdf

Measuring Innovation 2008: Squandered Opportunities

Firm level recommendations of measuring innovation. N=332 executives.

http://www.bcg.com/impact_expertise/publications/files/Measuring_Innovation_Aug_2008.pdf

Australian Bureau of Statistics - Tasmania (March 2008)

Measuring Innovation: Towards developing a scorecard

Surveys definitions and other measurement projects, including Schumpeter, Oslo Manual, output, outcome and input based measures, linkages and knowledge diffusion approaches. Assesses scorecards from OECD, European Innovation Scorecard, Canadian Scoreboard, Massachusetts, Progressive Policy Institute (WA.), Global Creativity Index. Creates Tasmanian scorecard with six categories: knowledge creation, human resources, finance, knowledge diffusion, collaboration in R&D, Market Outcomes.

http://www.abs.gov.au/AUSSTATS/abs@.nsf/Lookup/8163.6Main+Features12008?OpenDocument

or

Tuesday, November 11, 2008

Friday, August 22, 2008

Innovation and the Environment - Economist Debate

Economist debate: (Join in 19-29 Aug - link below)

My response...

Richard Ferrers, Innovation Researcher, University of Melbourne/Qld, www.valman.blogspot.com

Join the debate: 19 Aug - 29 Aug here

Thursday, July 10, 2008

iPhone Pricing (Out of this world) - Australia

Iphone launches tomorrow in Australia. And the deals are attractive, except for the data prices.

Optus, Telstra, and Vodafone are the carriers. I prefer the Optus deal, $39/mth, including 500Mb data, and a few calls. But the killer is the data pricing....

Be careful with data prices (Optus) in the fine print.

-------------------------------------------------------------------------

After the included data, prices are: $350 per Gb (ie $0.35 per Mb)

which equates to about one or two youtube music videos per day (10Mb) on the Optus $39 = 500Mb monthly plan. You could burn through that download with an hour or two of youtube viewing on the tram. I think a few parents of teenagers are going to be quite surprised when they get a bill for 20 hours of youtube viewing = approx. $70 per hour (10Mb/3min*20). Look forward to the Today Tonight stories on that.....

Other prices, once using up monthly limit are: Movie 350Mb ($100), Youtube music video 10Mb ($3.50), Large photo 1Mb ($0.35), Skype 150k/min ($0.06/min), Internet radio 1Mb/min ($0.35/min), software downloads 10Mb ($3.50) / 100Mb ($35), GPS similar to radio or skype prices.

However, 500Mb probably equates to unlimited text, and small photo downloads, so browsing, without large photos is effectively unlimited.

I'll be waiting until - either the download limit is shaped with no excess fees - or there is more like 1-2Gb included. At home I (my wife and I) use Virgin 4Gb/500k for $60 with local, and STD calls included (for comparison). I have Ipod Touch with no monthly fees, and free (ok $60) wifi at home.

Thursday, June 5, 2008

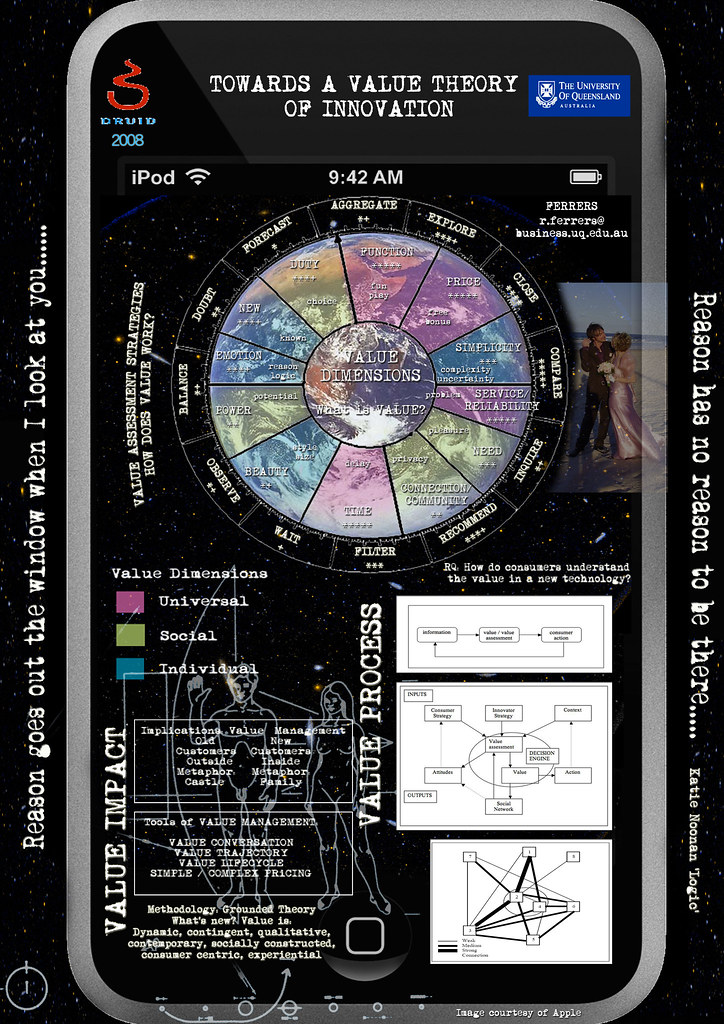

DRUID poster, Copenhagen Business School (17-20 June)

Full paper, including references here.

It's June (2008) and time for the DRUID conference on Innovation and Entrepreneurship.

Here are the summaries of the thesis in Poster form:

Here are the summaries of the thesis in Poster form:

One is in A1, and the second in A2.

These posters focus on (A1) the top level analysis: the value dimensions, the top level concepts, the value assessment strategies, the implications and tools of 'Value Management'.

The A2 poster, compares 'Value Management' with two pieces of literature, one from Innovation (Christensen 1997), and one from Customer Value (Zeithaml 1988), and outlines the interviewees, and shows the major references.

Tuesday, May 27, 2008

User Innovation Conference Invitation - Aug '08

You might be interested...! I was invited this week to attend a workshop on Open and User Innovation, hosted jointly by MIT, and Harvard Business School in Boston, 4-6 August.

See link to workshop - http://userinnovation.mit.edu/conf08/attendee/new

These workshops have been held on an invitation only basis since 2003, and about 50 academics attend annually who are pursuing research in this area. Application required writing on my research interests, PhD progress to date, and providing a CV. I am hoping to present a paper there too - still waiting to hear.

Three PhDs are going, including me, and two others - one from Zurich, and one from Holland.

Pretty cool hey! Now trying to squeeze the last dollars out of the budget allocated to me...to get me there...

See link to workshop - http://userinnovation.mit.edu/conf08/attendee/new

These workshops have been held on an invitation only basis since 2003, and about 50 academics attend annually who are pursuing research in this area. Application required writing on my research interests, PhD progress to date, and providing a CV. I am hoping to present a paper there too - still waiting to hear.

Three PhDs are going, including me, and two others - one from Zurich, and one from Holland.

Pretty cool hey! Now trying to squeeze the last dollars out of the budget allocated to me...to get me there...

Saturday, April 5, 2008

2% GST to fund - Low Carbon Incentive Scheme - Your say

Would you support:

- 2% extra GST to pay for and encourage clean transport and clean green power produced, or

- a carbon tax on petrol / new cars / electricity to encourage green power and transport.

Please add demographic [eg age, sex, location, income], and contact (if you wish).

1 page summary of proposal (pdf) [Update 11/4]: Final Garnaut Submission (pdf) [Update: 18/4] Included in The Australian Top 50 Ideas for 2020 Summit here #28

1 page Petition flyer (pdf) Full petition to print (pdf)

Thank you.

Richard Ferrers

Innovation Researcher

University of Queensland

Research Fellow, Centre for Global Innovation and Entrepreneurship

University of Melbourne

Friday, April 4, 2008

Low Carbon Incentive Scheme

I have been reviewing the Garnaut Emission Trading Scheme (ETS) Discussions paper, and am concerned of the potential failure of this policy to encourge low carbon (C) technology development as part of writing my Implications chapter of my PhD thesis (www.valman.blogspot.com).

I would encourage you to comment on my DRAFT submission (brief) below, and the attached key documents, from Garnaut, Foxon (Imperial College) which is excellent [technological lock in, technology trajectory], and Rayner (Nature - thanks ANDREW).

While the submissions are not due until next week, I am seeking comments from industry (Holden, Toyota, Electric vehicles mfger), consumers (my PhD interviewees), Govt (Vic summit 04.04.08, and QG), and academia (yourselves). This is an early draft, and I will insert innovation references, from my thesis in the next few days and recirculate. But thought a brief, but early draft would give you more time to comment.

I am sure you will be all very busy, and hence PhD students can give such matters more time, but I would encourage you to participate in this important process. Each generation has its problems to address, and I believe, for now, ours is climate change.

Any time and comments you could contribute would be much appreciated.

Thanks and regards

Richard Ferrers

University of Qld/Melbourne

Here are the four problems I see with the ETS, encouraging low C technology (also below):

Firstly, the ETS will encourage incremental innovation in power stations, and transfer from coal to gas, however it will not encourage radical or disruptive innovation, which is likely to come from small firms operating outside of the power and car/oil industries. Disruptors who do not hold C certificates have less incentive from the ETS to innovate.

Secondly, disruptive innovation can decrease the value of C certificates, giving certificate holders an incentive to resist such technology to protect the value of their investment in C certificates.

Thirdly, oil companies who purchase certificates, rather than petrol consumers, to keep the ETS simple, are more likely to pass C prices onto consumers, than to create or buy low C technology, which is outside their competencies, and would reduce their profits.

Fourthly, to protect their C lock in, the coal and oil industries have incentive to undermine the processes, and distract funding away from other low C technologies eg QLD $900M clean coal investments vs $26M Centre for Low Emission Technology, VIC $187M Energy technology innovation strategy (including $103.5M clean coal) vs $12M for renewable energy support fund,

Please see my suggested solution, a Low Carbon Incentive Scheme outlined below.

Thank you...

-----Original Message-----

From: Premier of Victoria [mailto:no-reply@premier.vic.gov.au]

Sent: Wed 02/04/2008 15:23

To: Richard Ferrers

Subject: Share Your Ideas

Thank you for your email to the Premier. A response will be sent to you as soon as possible.

Richard Ferrers

5/83 Park St

St Kilda West 3182

r.ferrers@business.uq.edu.au

03 9534 4830

0422 268 061

Idea:

Goals to transition to a low Carbon (C) economy:

- low C transport

- low C power

- low C exports

- low C workforce

The emission trading scheme (ETS) is a good start to get C prices into products, but greater incentive is needed to encourage success in low C technology, if we want to do so fast. The ETS is likely to take perhaps some 10-15 years to achieve this.

Some problems exist with the ETS encouraging low C technology. Firstly, the ETS will encourage incremental innovation in power stations, and transfer from coal to gas, however it will not encourage radical or disruptive innovation, which is likely to come from small firms operating outside of the power and car/oil industries. Disruptors who do not hold C certificates have less incentive from the ETS to innovate.

Secondly, disruptive innovation can decrease the value of C certificates, giving certificate holders an incentive to resist such technology to protect the value of their investment in C certificates.

Thirdly, oil companies who purchase certificates, rather than petrol consumers, to keep the ETS simple, are more likely to pass C prices onto consumers, than to create or buy low C technology, which is outside their competencies, and would reduce their profits.

Fourthly, to protect their C lock in, the coal and oil industries have incentive to undermine the processes, and distract funding away from other low C technologies eg QLD $900M clean coal investments vs $26M Centre for Low Emission Technology, VIC $187M Energy technology innovation strategy (including $103.5M clean coal) vs $12M for renewable energy support fund,

Therefore, to avoid these ETS problems, I suggest a Low C Incentive scheme, which collects funds and pays low C users and producers to encourage such use and production. Funding should be not at the expense of other government services (revenue neutral), and should encourage market solutions to low C needs. But the incentive should be paid 50% to producers and 50% to consumers to reward both parties.

Funds could be raised through a levy on petrol prices, and electricity bills. But consumers have told me, during a process of consultation, that this could place too heavy a burden on already stressed households. This could be a transitional arrangement (say two years) to be replaced by a broad ranging, but small, consumption tax. A level of 2%, added to GST, and collected in the same way, and with the same rules, could be collected by the ATO, then forwarded to the Carbon Bank (see Garnaut) for distribution to low C users and producers. Low income families would be protected as food would not be levied. And at a low 2% the impact would be slight on individual transactions. Also, business would not be levied, only consumers, reducing political issues, in selling the scheme to business. At 2%, funds of around $1B per month could be raised. Significantly ahead of Victoria\'s $200M action plan or Qld $900M investment in clean coal over ten years.

Payments should be made for results, not for R&D, so low C MWh of electricity would be paid from the fund, up to 50% of capital costs. Low C vehicles would be paid for out of the fund eg Toyota Prius, if they save 50% over normal vehicles.

Each month, receipts would be balanced with payments, so the fastest developers of low C technology were paid, starting a low C development race - a gold rush. Unspent receipts, would go to other C offset, such as planting trees, a portion could be saved (say 40%) for low C loans to buy solar heating, or fund low C R&D. A small proportion could fund R&D alone (say 20%), and administration (say 5%).

Funding could also come from sales of C certificates.

The fund should be spent on low C power (1/3), low C transport (1/3) and compensation to workers transitioning from high C to low C jobs(1/3). An incentive to leave high C jobs (say $10,000 per year of service, payable from fund in month of leaving or pro rata from funds available) and for employers to take on workers from high C jobs (say $10,000, payable half on hiring, and half on one year anniversary), into low C industries (ie receiving incentive payments).

See full details in submission to Garnaut review (April 11).

Richard Ferrers

Innovation Researcher

University of Queensland

Centre for Global Innovation and Entrpreneurship

University of Melbourne

Tuesday, March 11, 2008

DRUID Conference - Copenhagen, first Value Management Results paper

Hello all,

The first results paper on Value Management has been submitted to the DRUID conference in Copenhagen (June 2008) - www.druid.dk .

See paper on related website - thejoie.com.

Any comments appreciated.

Richard

Wednesday, January 30, 2008

Draft results release Nov '07 - another brick in the wall

See draft results (Release III) on Value Management:

Problem:

Generally, why do some innovations succeed and others fail?

Why the delay between invention and market acceptance of an innovation?

Specifically, and in depth - how do consumers understand the value in new technology?

And generally, how do consumers behave to assess, and communities make technology assessment decisions?

Recent Technology Impact - Explaining takeup of broadband, digital television, 3G mobile.

Practical Impact - Impact on marketing of technology, impact on understanding process of innovation.

Policy Impact - Australian election debate about political intervention in stimulating takeup of broadband by consumers.

Release II

Value supposed as explanation for innovation success, and spread of new technology.

Value defined as personal, subjective ascertainment of costs, benefits and risks.

Impact: Need for value management; tools: value trajectory, value conversation

Release III

What is value?

How does value work?

What should marketers, innovators, policy makers do about consumer value?

What is value?

Figure 1 - Value in action - the simplest view: Value as a black box.

In Figure 1, value is a mediator between information and consumer action. Action includes inaction or waiting, and value assessments are stored in attitudes, that can lead to future action.

Figure 2 - Opening the black box of value. Value comprises several interacting concepts.

Value was found to be very multi-faceted. Over 80 value elements were found that compete against each other to assess value. These were compressed into 12 value dimensions. Four of these dimensions were agreed by 100% of interviewees. The remaining eight dimensions, were noted by between 1/3 and 2/3 of interviewees.

Value Dimensions are a continuum of opposites, with one end of the dimension increasing value, and the other end decreasing value. Value is sensitive to new information, and new information is assessed as to its impact on value dimensions, leading to a new value assessment. Some people prefer one end of the dimension, while others may prefer the other end. For instance, some prefer new things, others prefer what they know already, and don't like to change. Some people may take different positions for different things. Some prefer simple, others complicated. But value dimensions compete with each other - simplicity and function, price and reliability, beauty and community, privacy and knowledge.

Key Dimensions:

Function Price Time / convenience Service / reliability

Other Value Dimensions: (from most to least common)

Learning / new Emotion Need Simplicity / Complexity

Duty Power / Freedom Connection / Community Beauty / aesthetics

Further questions:

How does value work? ... to follow

What should you do about value? ... to follow

Subscribe to:

Posts (Atom)

{kind=link}

{kind=link}

{kind=link}